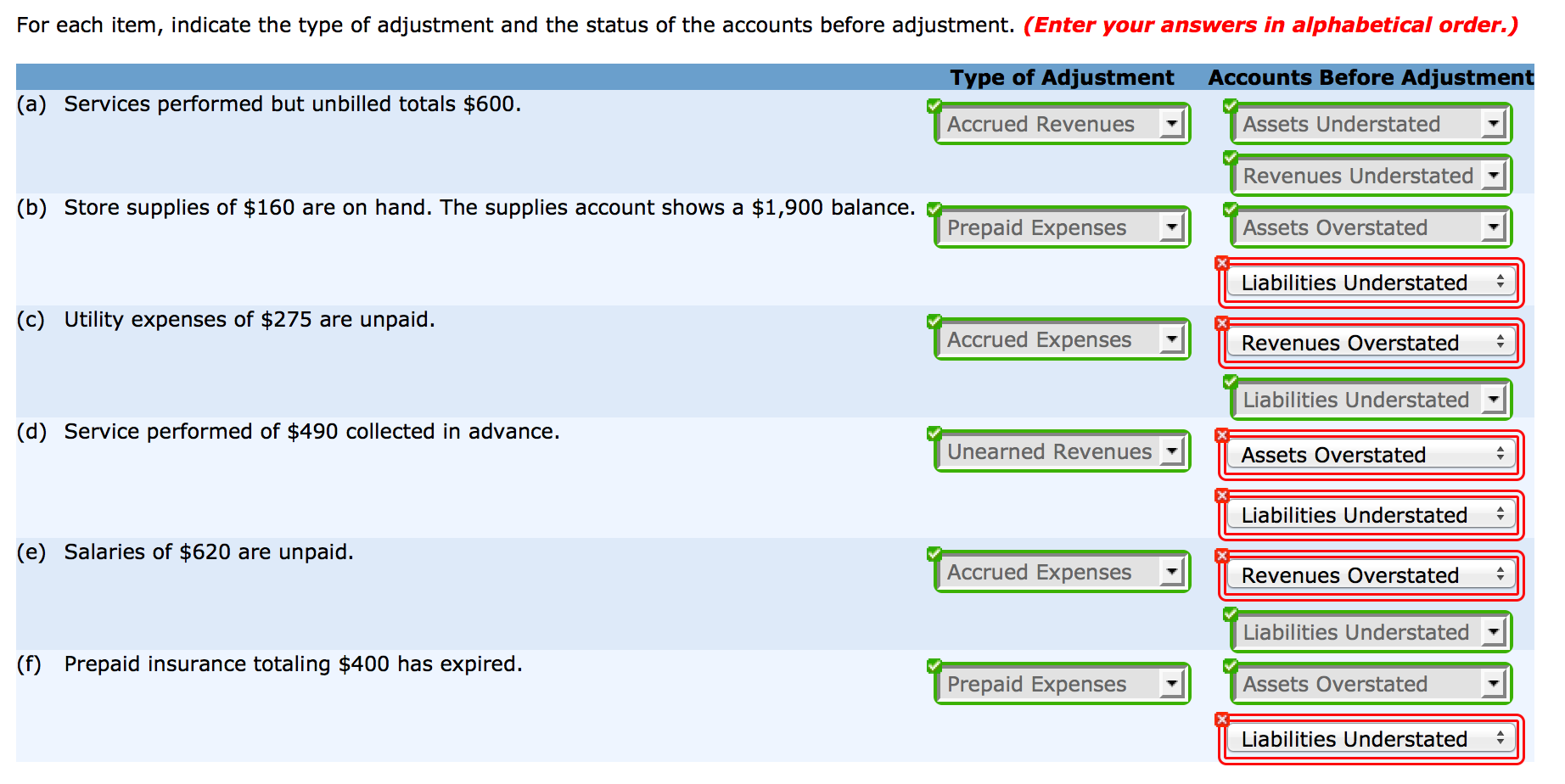

The new Federal Set-aside aggressively fasten financial plan into the 2022, answering highest and you may persistent inflation. The new resulting credit cost improve having property and you will enterprises was fundamentally expected. Although not, fixed-price financial interest levels was basically particularly sensitive to the insurance policy routine alter.

We find you to definitely interest rate volatility in addition to novel characteristics of financial instruments was indeed extremely important members in order to last year’s outsized home loan rates motions.

Given easily fasten economic plan

New Government Put aside first started the present day financial coverage duration at their fulfilling by increasing the federal loans speed target by 0.twenty-five commission affairs, to 0.250.50 %. Due to the fact inflation remained persistently elevated, the newest main financial proceeded training the target during the next conferences. The pace stood during the cuatro.254.50 percent in the seasons-prevent.

The fresh new Federal Reserve views changes for the government fund rate’s target variety as the top manner of modifying monetary plan. But not, the new central financial and additionally been decreasing the measurements of its balance sheet-that has Treasuries and you can financial-supported bonds-for the by limiting reinvestment regarding principal repayments to the the maturing holdings.

The reaction off long-name interest rates to this firming period has been faster obvious compared to escalation in the insurance policy rate. The fresh 10-season Treasury speed come 2022 around americash loans Perdido 1.6 percent, peaked at around cuatro.dos % in later Oct, and you can stood at almost step 3.8 percent at season-end. Very, since the federal fund price target went upwards 375 base factors (step 3.75 payment things), the benchmark enough time-term Treasury rate moved right up simply 220 foundation factors.

One might imagine you to definitely mortgage loan prices do directly track much time-name Treasury cost. You to definitely was not the truth (Graph 1).

The common 29-season repaired-rate financial began 2022 at the step three.one percent, peaked in later October on eight.one percent and you will finished the entire year in the 6.4 percent. When you find yourself each other 10-year Treasuries and you may mortgage loans increased over the year, its distinction was 60 foundation affairs in the beginning of the year, widened to as much as 190 basis products during the October, and you will stood during the 150 basis circumstances at season-prevent. What accounts for the important expanding between them?

Decomposing home loan interest levels

Mortgage interest levels you to homes spend to get otherwise refinance house have been called top rates. A generally quoted measure of such rates comes from Freddie Mac’s Top Mortgage Markets Questionnaire, the information and knowledge origin for Chart step one. So it per week report has got the mediocre interest levels to own very first-lien traditional, conforming fixed-price mortgage loans with financing-to-value of 80 per cent. Conventional compliant mortgage loans are those entitled to securitization-otherwise resale so you can people-owing to Freddie Mac and Federal national mortgage association. Those two government-sponsored people (GSEs) accounted for almost 60 percent of new mortgages throughout the 2022.

The basis to possess primary pricing ‘s the supplementary-business interest rates reduced so you’re able to traders carrying uniform mortgage-backed securities (UMBS) guaranteed by Fannie mae otherwise Freddie Mac. UMBS are built and you may replaced having deals (focus costs in order to dealers) from inside the 50-basis-area increments. Brand new additional price in keeping with a beneficial UMBS at par value (typically, face value) is known as the newest voucher rate.

Graph dos screens the main-mortgage-field rate (just what homeowners shell out) in addition to additional-. The essential difference between both series-or even the primarysupplementary give- reflects several products.

Very first, all of the old-fashioned compliant home loan borrowers spend twenty five base affairs to own loan repair. Second, Fannie mae and you may Freddie Mac charges ensure charges to be sure punctual commission regarding principal and you can attention with the UMBS. Ultimately, financing originators need coverage its will cost you, together with income for the collateral, which may vary over time because of home loan consult. The mainadditional spread, which averaged around 105 basis activities throughout the 2022, don’t exhibit a trend which will account for the fresh widening relative to a lot of time-title Treasury pricing into the months.

Chart 2 depicts that large boost in pri is actually motivated by secondary-field costs. Conceptually, one can think of secondary-market pricing as the highlighting the sum an extended-name risk-100 % free speed (having benefits, i tell you the 10-seasons Treasury price) in addition to cost of a call alternative which enables individuals so you can prepay their mortgages when without punishment.

It continuous prepayment choice is costly to loan providers because it’s resolved more often whether or not it experts new debtor from the debts of financial, since the individuals re-finance to your straight down-price fund. The difference between the fresh secondary-markets rate and you will lengthened-dated Treasury pricing shall be looked at as the price of new prepayment solution.

Rate of interest volatility widens mortgage develops

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/cmg/GTOKB4YZM5EABA7JXTVWPUDNRY.jpg)

Solution thinking raise on the volatility of your own underlying asset value. Simply because higher volatility increases the opportunities the asset’s rates will visited an even that produces the possibility rewarding. In this case, financial prepayment options flower during the worthy of on account of enhanced underlying attention speed volatility.

Graph 3 plots the difference between the newest second-mortgage-industry price reduced the 10-year Treasury rate up against a generally quoted way of measuring interest rate volatility- this new Flow index. This new Circulate directory songs the amount of Treasury rates volatility more a month which is implied of the choice towards Treasury securities. Instance choice-required price volatility will be regarded as reflecting suspicion in the the near future highway regarding underlying interest levels.

Increased suspicion regarding the future path of Treasury rates more than far away from 2022 translated on the improved opinions of your own home loan prepayment solution, improving new pass on anywhere between financial-supported securities and you may enough time-dated Treasuries. Since e well informed regarding the future path of interest prices from the season-end 2022, option-intended Treasury volatility dropped, plus the pass on between home loan-recognized securities and you will Treasuries implemented.

The latest character of great interest rate suspicion

As the rise in financial costs throughout 2022 was generally determined by the boost in chance-100 % free Treasury costs, it actually was amplified by grows about cost of the mortgage prepayment solution, hence reflected broader suspicion about the coming roadway interesting pricing.